“These three blue chip stocks lost investors over 60%. The names will surprise you.”

There is a belief that runs deep in the Indian retail investor’s mind: blue chip stocks don’t really hurt you.

You hear it at family dinners. You read it in introductory investing guides. You believe it when your broker says, “Sir, yeh toh Nifty 50 mein hai.”

The logic feels sound. Blue chip companies are large, established, well-managed businesses with strong brands, loyal customers, and decades of track record. They are supposed to be the safe harbour when markets get rough.

But the data says something uncomfortable: even the most well-known, widely-held, institutionally-loved companies in India can — and do — destroy enormous amounts of investor wealth. Not by a little. Sometimes by 60%, 70%, even 95%.

Here are three real cases from the Indian market. Each company was considered a blue chip. Each had millions of retail investors. And each delivered losses that most people associate only with penny stocks or speculative bets.

What Is a Blue Chip Stock, Really?

Before we get into the cases, let’s be clear about what we mean by “blue chip.”

In the Indian context, a blue chip stock typically refers to a company that is:

- Listed on the Nifty 50 or Sensex (or was at some point)

- Part of a well-known business group or sector leader

- Covered extensively by institutional analysts

- Widely held by mutual funds, FIIs, and retail investors

- Perceived to be “safe” relative to smaller, lesser-known companies

None of the three companies below are obscure. None were speculative darlings. All three were, at various points, held by crores of retail investors who trusted the blue chip label.

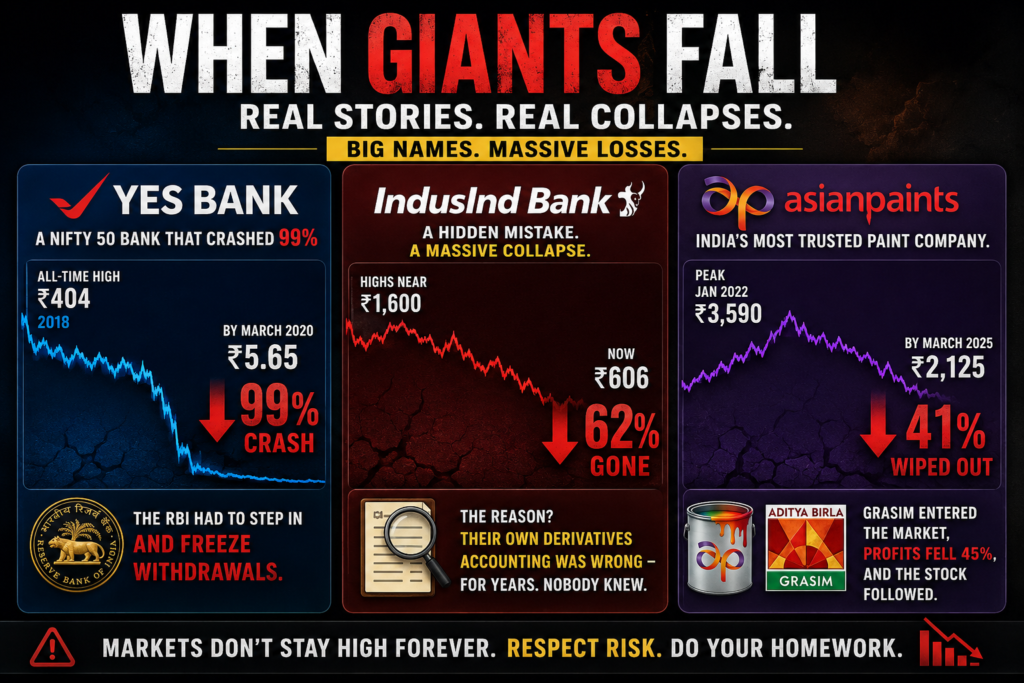

Case 1: Yes Bank — From ₹404 to ₹5.65 (–99%)

Peak: ₹404 (August 2018) Trough: ₹5.65 (March 2020) Fall from peak to trough: ~98.6% Total investor wealth destroyed: Tens of thousands of crores

The Blue Chip Story

If you had asked any informed investor in 2016 or 2017 to name India’s most aggressive and exciting private sector bank, Yes Bank would have been near the top. Founded in 2003 by Rana Kapoor and Ashok Kapur, the bank grew at a breathtaking pace. It became India’s sixth-largest private bank by assets. Its loan book swelled. Its stock soared. At its peak in August 2018, Yes Bank touched an all-time high of ₹404 per share — giving it a market capitalisation in the range of ₹90,000+ crore.

It was a Nifty 50 component. Mutual funds were holding it. Analysts were publishing bullish reports. Retail investors were adding it to their “safe” portfolios.

What Went Wrong

Behind the growth story was a collapsing quality of lending. Yes Bank had been aggressively extending credit to stressed corporate borrowers — groups that more conservative lenders had already turned away. The bank was also under-reporting its Non-Performing Assets (NPAs) to the RBI. When the regulator forced recognition of these stressed loans, the numbers were alarming.

Gross NPAs shot up to 17.3% of the loan book by March 2020 — meaning roughly one in every six rupees lent was unlikely to come back. The RBI, in an unprecedented move, imposed a moratorium on Yes Bank in March 2020, capping customer withdrawals at ₹50,000. This was the kind of restriction Indians associate with failing cooperative banks — not a Nifty 50 private bank.

Rana Kapoor, the bank’s co-founder and long-serving CEO, was arrested in 2020 on charges of money laundering and fraud. A rescue plan was put together involving SBI and other banks, but the stock — by then — had fallen to ₹5.65. That is a fall of approximately 99% from the 2018 peak.

An investor who put ₹10 lakh into Yes Bank at its all-time high saw that investment become roughly ₹14,000 in under two years.

The Lesson

The Yes Bank collapse shows that brand, size, and Nifty 50 membership are not the same as financial health. The critical variables — loan quality, promoter integrity, and regulatory relationship — were deteriorating for years while the stock kept climbing on momentum. By the time retail investors noticed the danger, the damage was already done.

Today, as of mid-2026, Yes Bank trades around ₹20 — still roughly 95% below its 2018 peak. Recovery has been slow and grinding.

Case 2: IndusInd Bank — From ~₹1,600 to Below ₹600 (–62%)

Peak: ~₹1,597 (February 2020, pre-COVID highs) Trough (recent): ₹606 (52-week low, 2025) Fall from peak area: Over 62%

The Blue Chip Story

IndusInd Bank is a different kind of story — one that shows how a bank can be genuinely well-run for years, earn a stellar reputation, appear on “quality banking” lists, and still inflict serious pain on its investors.

Founded in 1994 and promoted by the Hinduja Group, IndusInd Bank was considered one of India’s most efficiently run private sector banks. It was known for sharp management, healthy NIMs (Net Interest Margins), and well-diversified retail lending. It was a Nifty 50 stock. Institutional investors loved it.

What Went Wrong

The slide began with COVID-19 in early 2020, which hit the bank hard given its exposure to vehicle loans and microfinance — segments where borrowers were severely impacted by lockdowns. But the bank appeared to recover, and investors who bought the dip saw some recovery.

The deeper shock came in March 2025. An internal audit revealed that IndusInd Bank had been miscalculating hedging costs on past foreign exchange derivative transactions for several years. The bank disclosed this discrepancy, estimating an impact of ₹1,600–2,000 crore on net worth — roughly 2.35% of its December 2024 net worth. What made investors panic was not just the quantum of the loss, but what it implied: that the bank’s internal controls and risk management were weaker than the market had assumed.

The stock fell over 20% in a single session on March 11, 2025 — a day that Groww data described as the largest single-day fall for the stock since March 2020. Mutual funds collectively lost over ₹6,000 crore in a day. The stock continued to slide, hitting a 52-week low of ₹606 in 2025. From its peak near ₹1,600, that was a fall of over 62%.

The stock has since partially recovered, trading near ₹920–930 in mid-2026, but investors who bought near the highs are still sitting on substantial paper losses.

The Lesson

IndusInd Bank illustrates a specific risk that applies even to well-managed companies: accounting and governance risk. The bank was not reckless in its lending. Its loan book was not full of bad debts like Yes Bank. But an internal process failure — years of miscalculated hedging costs — was enough to destroy over 60% of market cap from peak to trough. In banking, trust is the product. When trust breaks, the fall is fast.

Case 3: Asian Paints — From ₹3,590 to Below ₹2,125 (–41%) and Still Under Pressure

Peak: ₹3,590 (January 10, 2022) Trough (52-week low): ₹2,124.75 (March 2025) Fall from all-time high to trough: ~40.8% Earnings decline: Net profit fell 45% YoY in Q4 FY25; down 32.8% for full FY25

Note: While Asian Paints’ peak-to-trough is ~41% and not yet 60%, it merits deep examination as an ongoing blue chip destruction story — and the fundamentals suggest the pressure is not yet fully resolved.

The Blue Chip Story

If you built a shortlist of the five most iconic Indian consumer stocks of the last two decades, Asian Paints would be on almost every list. Founded in 1942, India’s largest paint company had created what investors call a “compounding machine” — consistent volume growth, strong pricing power, dominant market share (near 60%), enviable return on equity, and a promoter family with deep skin in the game.

For two decades, buying Asian Paints and holding it was considered almost as safe as an index fund — except that it beat the index consistently. Retail investors revered it. Mutual funds were overweight on it. At its peak of ₹3,590 in January 2022, it had a market capitalisation of roughly ₹3.44 lakh crore.

What Went Wrong

Asian Paints’ decline is not a scandal or fraud story. It is something arguably more unsettling: the erosion of a competitive moat in slow motion.

Three forces converged:

1. Raw material inflation: Crude oil derivatives account for nearly 50% of paint raw materials. The Russia-Ukraine war sent crude prices soaring, compressing Asian Paints’ margins even as it passed on price increases to consumers.

2. Demand weakness: Higher prices and general macroeconomic uncertainty hit housing-linked discretionary spending. Volume growth — the engine of Asian Paints’ earnings — decelerated meaningfully.

3. The Grasim disruption: This is the big one. Aditya Birla Group’s Grasim Industries entered the decorative paint market with its Birla Opus brand, backed by a committed capital expenditure of ₹10,000 crore. Leveraging existing distribution through UltraTech Cement dealerships and the Birla White brand, Grasim rapidly took market share. Asian Paints’ domestic market share reportedly slipped from approximately 59% to around 52% within a year of Birla Opus gaining scale.

The impact showed up brutally in earnings. In Q4 FY25, Asian Paints reported a net profit of ₹692 crore — down 45% year-on-year and significantly below analyst estimates. Full-year FY25 net profit was down 32.8%, with revenue also declining 4.5% — the first revenue contraction in years.

The stock fell from ₹3,590 to a 52-week low of ₹2,124.75 in March 2025. That’s a 40.8% peak-to-trough decline for a company that was considered untouchable.

As of mid-2026, Asian Paints trades around ₹2,600–2,700, still more than 25% below its all-time high, while the broader Sensex has largely recovered.

The Lesson

Asian Paints teaches perhaps the most nuanced lesson of the three: moats can be eroded, and premium valuations compress painfully when they do. Investors who bought at ₹3,590 were paying a very high price for assumed perpetual dominance. When that dominance was challenged, the price fell — even though the underlying business is still profitable and fundamentally sound. In investing, the price you pay is as important as the quality you buy.

The Connecting Thread: Why “Blue Chip” Is Not a Risk Category

Looking at these three cases together, a pattern emerges.

Each company was widely held and covered. Each was considered low-risk by conventional wisdom. And each taught investors a different variant of the same lesson — that the label “blue chip” describes scale and reputation, not safety.

Yes Bank showed that a banking stock can go to near-zero if governance and credit quality break down — and the signs are often invisible until it’s too late.

IndusInd Bank showed that even genuinely well-managed banks carry hidden operational and accounting risks that can emerge suddenly, destroying 60%+ of value in a matter of weeks.

Asian Paints showed that businesses built on competitive moats can see those moats challenged, and premium-priced stocks face brutal drawdowns when earnings disappoint even slightly.

What Should Retail Investors Take Away?

This post is not a call to avoid large-cap stocks. Indian blue chips have created enormous wealth over long periods. HDFC Bank, Titan, Infosys, and many others have rewarded patient investors handsomely.

The takeaway is more specific:

1. Diversify within your “safe” allocation. Concentration in even one or two blue chip names creates meaningful single-stock risk. A diversified portfolio of 15–20 stocks across sectors is safer than 5 “good names.”

2. Watch earnings trends, not just the stock price. All three stories above had earnings warning signs — NPA build-up at Yes Bank, NIM compression at IndusInd, volume deceleration at Asian Paints — that preceded the stock price crash. Train yourself to read quarterly results.

3. Understand what you are paying for. A company with strong fundamentals trading at 70x earnings is not the same risk as the same company at 25x earnings. The multiple you pay matters enormously to your eventual returns and loss potential.

4. Never confuse brand familiarity with fundamental safety. You know the name. You use the product. You trust the company. None of that tells you whether the stock is safe to buy at the current price.

5. Diversify across asset classes. Even the most sophisticated institutional investors diversify across equities, debt, gold, and real assets. Your entire net worth should not depend on your equity picks being right.

A Final Thought

The Indian retail investor has come a long way. SIP volumes are at record highs. Demat accounts have crossed 17 crore. Financial literacy is genuinely improving.

But there is still a persistent blind spot: the belief that size equals safety.

These three companies — a bank that the RBI had to rescue, a bank that misreported its own books for years, and a paint company that lost market share to a new entrant — prove otherwise.

Blue chips are not immune to failure, competition, or governance breakdowns. Knowing this is not a reason to be fearful. It is a reason to be thoughtful, diversified, and honest about risk — which is exactly what long-term wealth creation requires.

Disclaimer: This post is for educational purposes only and does not constitute investment advice. Past performance of any stock is not indicative of future returns. Please consult a SEBI-registered investment advisor before making any investment decisions.

All historical price data referenced in this post has been sourced from publicly available market databases including TradingView, Screener.in, Groww, and company filings.